These trends highlight a critical gap. Insurers are not lacking data, but they are lacking the ability to activate it in real time.

Traditional Customer 360 systems attempted to solve this problem by unifying data. However, unification without intelligence does not deliver business outcomes. A new approach is required, one that combines AI-native architecture, machine learning, and Digital Twin Intelligence to transform how insurers operate.

Why Traditional Customer 360 Falls Short in General Insurance

Traditional Customer 360 implementations often fail to deliver impact because they are built on outdated assumptions about how data should be processed and used.

-

Static Customer Profiles Limit Decision-Making

Most systems rely on batch updates and historical data, which results in outdated customer views. This limits the ability to act in real time and reduces the relevance of engagement.

Common limitations include:

- Customer profiles updated periodically instead of continuously

- Decisions based on past behavior rather than future intent

- Inability to respond instantly to customer actions

-

Fragmented Intelligence Across Functions

Even when data is consolidated, intelligence remains siloed across departments. This creates inconsistency in decision-making and customer experience.

- Marketing operates on campaign-level insights

- Claims teams lack full interaction context

- Underwriting relies on incomplete risk signals

- Customer service lacks a unified view of history

This fragmentation leads to inefficiencies and missed opportunities across the value chain.

-

AI as an Add-On Instead of a Core Capability

Many legacy systems introduce AI as a secondary layer, which limits its effectiveness.

- AI models operate in isolation

- Insights require manual interpretation

- Limited scalability across use cases

As a result, insurers struggle to fully leverage predictive capabilities.

-

Reactive Rather Than Predictive Operations

Traditional systems focus on reporting past events rather than predicting future outcomes. This makes it difficult to:

- Identify churn risks early

- Recommend the right products

- Optimize engagement timing

-

Lack of Continuous Learning

Customer behavior evolves constantly, but most systems do not adapt.

- No feedback loop from campaigns

- Limited learning from customer interactions

- Declining accuracy of insights over time

What AI-Native Customer 360 Means in Insurance

AI-native Customer 360 represents a shift fromh

-

Key Capabilities of AI-Native Architecture

AI-native platforms differ from traditional systems in several important ways:

- Intelligence embedded across the system

AI is integrated into data processing, identity resolution, segmentation, and activation - Real-time data processing

Streaming data replaces batch updates, enabling instant decision-making - Unified intelligence layer

All teams operate on the same real-time customer view - Predictive and prescriptive capabilities

Systems not only predict outcomes but also recommend actions - Continuous learning loops

Every interaction improves future predictions

This approach transforms Customer 360 into a dynamic intelligence engine that drives business outcomes.

- Intelligence embedded across the system

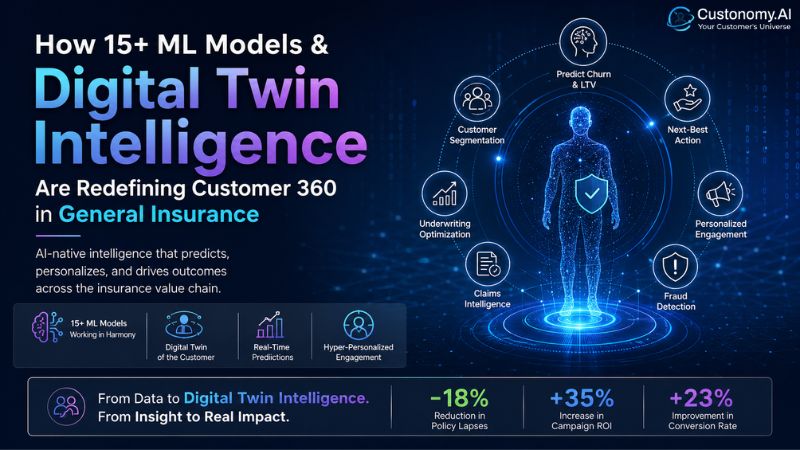

The Role of 15+ ML Models Working Together

Custonomy’s architecture is built on a multi-model approach, where more than 15 machine learning models work together to create a unified intelligence system.

-

Why Multi-Model Intelligence Matters

Customer behavior is influenced by multiple factors, including:

- Policy history

- Claims behavior

- Digital interactions

- Lifecycle stage

- External signals

A single model cannot capture this complexity effectively. Multiple models working together provide a more accurate and holistic understanding.

-

Key ML Capabilities

Custonomy leverages different models to solve specific business problems:

- Churn prediction models

Identify customers likely to lapse and enable proactive retention - Customer lifetime value models

Prioritize high-value customers for targeted engagement - Propensity and affinity models

Predict product preferences and buying intent - Next-best-action models

Recommend optimal engagement strategies - Fraud detection models

Identify anomalies across claims and behavior - Dynamic segmentation models

Enable real-time grouping based on behavior and context

- Churn prediction models

-

From Individual Models to an Intelligence Ecosystem

The real power lies in orchestration.

- Models continuously share insights

- Predictions are refined in real time

- Decisions are based on combined intelligence

This creates a system where intelligence is not fragmented but unified across the organization.

Digital Twin of the Customer: A New Paradigm

The Digital Twin of the Customer represents a significant advancement in Customer 360.

-

What is a Digital Twin

A Digital Twin is a dynamic and continuously evolving representation of a customer that combines data from multiple sources into a single intelligence layer

This includes:

- Policy data

- Claims history

- Interaction data

- Behavioral signals

- Digital activity

- Third-party data

-

What Makes Digital Twin Intelligence Powerful

Digital Twin Intelligence enables insurers to:

- Track customer state in real time

- Simulate customer journeys before execution

- Deliver context-aware personalization

- Continuously refine predictions

Explore how Custonomy can help you build a real-time, AI-powered intelligence foundation for general insurance.

How It Transforms Customer Understanding

Traditional profiles are static snapshots. Digital Twins are dynamic systems.

- Profiles show what happened

- Digital Twins predict what will happen next

This shift enables insurers to move from reactive engagement to proactive strategy.

Real-Time Predictions That Transform Insurance Operations

AI-native architecture combined with ML models enables real-time predictive intelligence across key areas:

-

Key Predictive Capabilities

- Churn prediction

Identify at-risk customers and trigger timely interventions - Customer lifetime value prediction

Optimize resource allocation and engagement strategies - Next-best-action recommendations

Guide interactions with precision - Fraud detection

Identify suspicious patterns early - Engagement prediction

Improve campaign effectiveness and conversion rates

- Churn prediction

Business Impact Across the Insurance Value Chain

The shift to an AI-native Customer 360 is not just a technology upgrade. It fundamentally changes how every function within an insurance organization operates. When intelligence becomes real time, unified, and predictive, it enables teams to move from reactive execution to proactive decision-making.

This transformation creates measurable impact across the entire insurance value chain.

-

Retention and Growth

Customer retention is one of the most critical levers for profitability in insurance. However, traditional approaches rely heavily on reactive engagement, often reaching out to customers only when renewal is imminent or after signs of disengagement are already visible.

AI-native Customer 360 changes this dynamic by enabling early detection of churn signals and proactive intervention.

- Identify policyholders at risk of lapse using behavioral, engagement, and policy signals

- Trigger personalized renewal journeys tailored to customer preferences and lifecycle stage

- Prioritize high-value customers using predictive lifetime value models

- Deliver timely nudges through the most effective channels

This approach allows insurers to engage customers before dissatisfaction escalates. Even small improvements in retention can significantly impact profitability, as retaining an existing customer is far more cost-effective than acquiring a new one.

-

Sales and Cross-Sell

Insurance growth increasingly depends on the ability to deepen relationships with existing customers rather than relying solely on new acquisitions. However, without clear visibility into customer needs and intent, cross-sell and upsell efforts often remain generic and ineffective.

With AI-driven intelligence, insurers can shift toward precision selling.

- Recommend products based on real-time behavior, policy history, and life events

- Identify high-propensity customers who are more likely to convert

- Prioritize leads using predictive scoring models

- Equip agents with complete customer context before every interaction

This enables sales teams and agents to move from reactive conversations to insight-led engagement. As a result, interactions become more relevant, conversion rates improve, and overall customer lifetime value increases.

-

Underwriting

Underwriting is a data-intensive function that relies on accurate risk assessment and pricing decisions. Traditional underwriting processes often depend on limited or outdated data, which can lead to suboptimal pricing and increased exposure to risk.

AI-native Customer 360 enhances underwriting by providing a more comprehensive and dynamic view of the customer.

- Enrich risk profiles using behavioral, demographic, financial, and third-party data

- Identify emerging risk patterns through continuous data analysis

- Improve pricing accuracy by incorporating real-time signals

- Enable faster underwriting decisions with pre-filled, data-driven insights

This leads to more precise risk evaluation and better alignment between pricing and actual risk exposure. It also reduces manual effort and accelerates decision-making processes.

-

Claims

Claims processing is one of the most critical touchpoints in the customer journey. It directly impacts customer satisfaction and trust. However, claims teams often operate with incomplete information, which leads to delays and repetitive processes.

AI-native Customer 360 transforms claims handling by providing full context and intelligent automation.

- Give claims teams access to complete customer history, including policies, interactions, and documents

- Route claims based on urgency, value, and risk profile

- Reduce the need for customers to repeat information across touchpoints

- Automate workflows to improve efficiency and reduce processing time

This results in faster claim resolution, improved operational efficiency, and a more seamless customer experience during moments that matter most.

-

Marketing Efficiency

Marketing in insurance has traditionally relied on broad segmentation and generic campaigns. This often leads to wasted spend and low engagement.

With AI-native Customer 360, marketing becomes highly targeted and data-driven.

- Build precise audience segments using real-time behavioral and policy data

- Deliver personalized campaigns across digital and offline channels

- Optimize timing, messaging, and channel selection using predictive insights

- Continuously refine campaigns based on performance data

This level of precision significantly improves campaign effectiveness while reducing unnecessary spend. It ensures that marketing efforts are focused on customers who are most likely to engage and convert.

-

Fraud Prevention

Fraud remains a significant challenge for insurers, with evolving patterns making it increasingly difficult to detect using traditional rule-based systems. Fraud often goes unnoticed when data is fragmented across systems.

AI-native Customer 360 enables a more proactive and comprehensive approach to fraud detection.

- Analyze multi-channel data, including claims, behavior, and interactions

- Identify anomalies and suspicious patterns in real time

- Strengthen risk assessment with enriched customer context

- Reduce false positives by using advanced machine learning models

This improves the accuracy of fraud detection while reducing financial losses and operational risk. It also enhances compliance by ensuring better visibility and traceability of data.

-

From Customer Data to Customer Intelligence

The insurance industry is moving toward a model where competitive advantage is defined by the ability to act on data in real time. Data alone does not create value. Value is created when data is transformed into intelligence that can drive decisions.

To achieve this, insurers need a strong foundation built on four key pillars.

What This Transformation Requires

- Unified data

All customer data from policies, claims, interactions, and digital channels must be consolidated into a single, reliable view - AI-native processing

Intelligence must be embedded into the system, enabling real-time analysis and decision-making - Continuous learning

Systems must evolve with every interaction, improving accuracy and relevance over time - Predictive intelligence

Insights must move beyond reporting to predicting future behavior and recommending actions

How Custonomy Enables This Shift

Custonomy bridges the gap between data and intelligence by combining advanced machine learning models with Digital Twin technology.

It enables insurers to:

- Unify fragmented data across all touchpoints into a single customer view

- Apply 15+ machine learning models to generate real-time insights

- Create a Digital Twin of each customer that evolves continuously

- Activate intelligence across marketing, sales, underwriting, claims, and service

Instead of relying on static reports, insurers gain access to a dynamic intelligence system that supports decision-making at every stage of the customer lifecycle.

From Storage to Intelligence Activation

Traditional systems focus on storing and organizing data. Modern platforms like Custonomy focus on activating intelligence.

- Data becomes actionable

- Insights become predictive

- Decisions become proactive

This shift allows insurers to move beyond operational efficiency and unlock new opportunities for growth, personalization, and customer engagement.

Conclusion: The Future of Insurance Belongs to Intelligent Systems

The general insurance industry is at a point where incremental improvements are no longer enough. Customer expectations are rising, competition is intensifying, and the pace of change continues to accelerate. In this environment, relying on fragmented data and static customer views limits both growth and innovation.

Customer 360 must evolve from a reporting layer into a real-time intelligence system that can understand, predict, and act. This is where AI-native architecture, multi-model machine learning, and Digital Twin Intelligence come together to redefine what is possible.

Insurers that embrace this shift gain the ability to:

- Anticipate customer needs instead of reacting to them

- Personalize every interaction based on real-time context

- Improve retention, conversion, and customer lifetime value

- Strengthen underwriting, claims, and fraud detection with deeper insights

- Align all functions around a single, continuously evolving customer view

This is not just a technology upgrade. It is a transformation in how decisions are made across the organization.

Custonomy enables this transformation by turning fragmented data into a living intelligence system. With 15+ machine learning models working together and a Digital Twin of every customer, insurers can move from static profiles to dynamic, predictive intelligence that drives measurable business outcomes.

The competitive advantage in insurance will no longer come from having more data. It will come from the ability to activate that data in real time and translate it into smarter decisions.

Organizations that adopt this approach will be better positioned to lead in a market defined by personalization, speed, and intelligence. Those that continue to rely on traditional systems risk falling behind.

Unlock the Full Potential of Your Customer Data

Turn fragmented policyholder data into real-time, AI-driven intelligence that powers growth, retention, and smarter decisions.